OpenAI's Deployment Company Is a Lock-In Machine, Not a Consulting Firm

DeployCo solves OpenAI's commoditization problem, not your deployment problem, and the lock-in is by design.

Core argument

The short version of the piece before you go deeper.

DeployCo solves OpenAI's commoditization problem, not your deployment problem, and the lock-in is by design.

# OpenAI's Deployment Company Isn't Consulting. It's the Most Aggressive Lock-In Play in Enterprise AI History

OpenAI just told you everything you need to know about where the enterprise AI market is headed. Most people missed it.

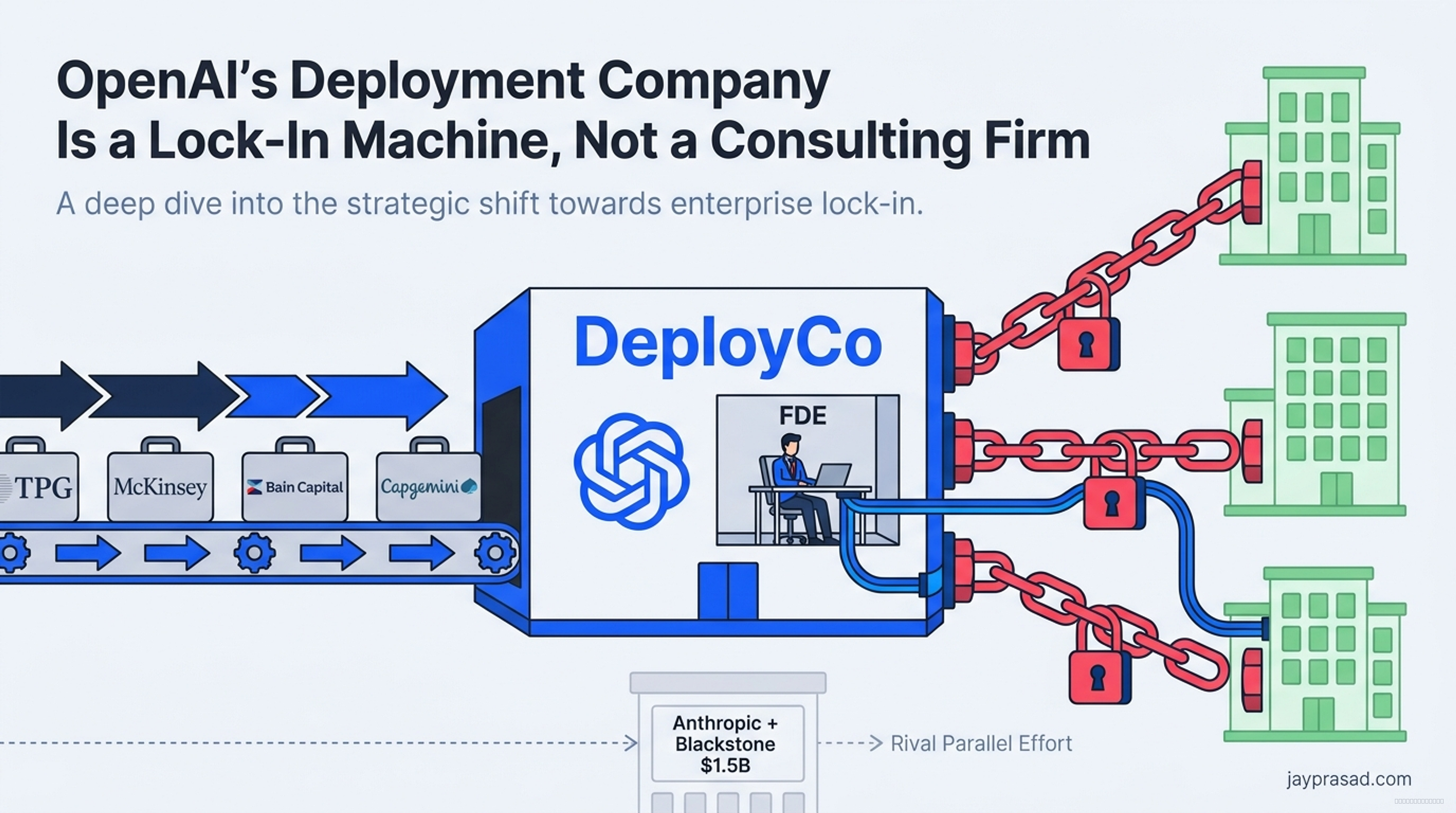

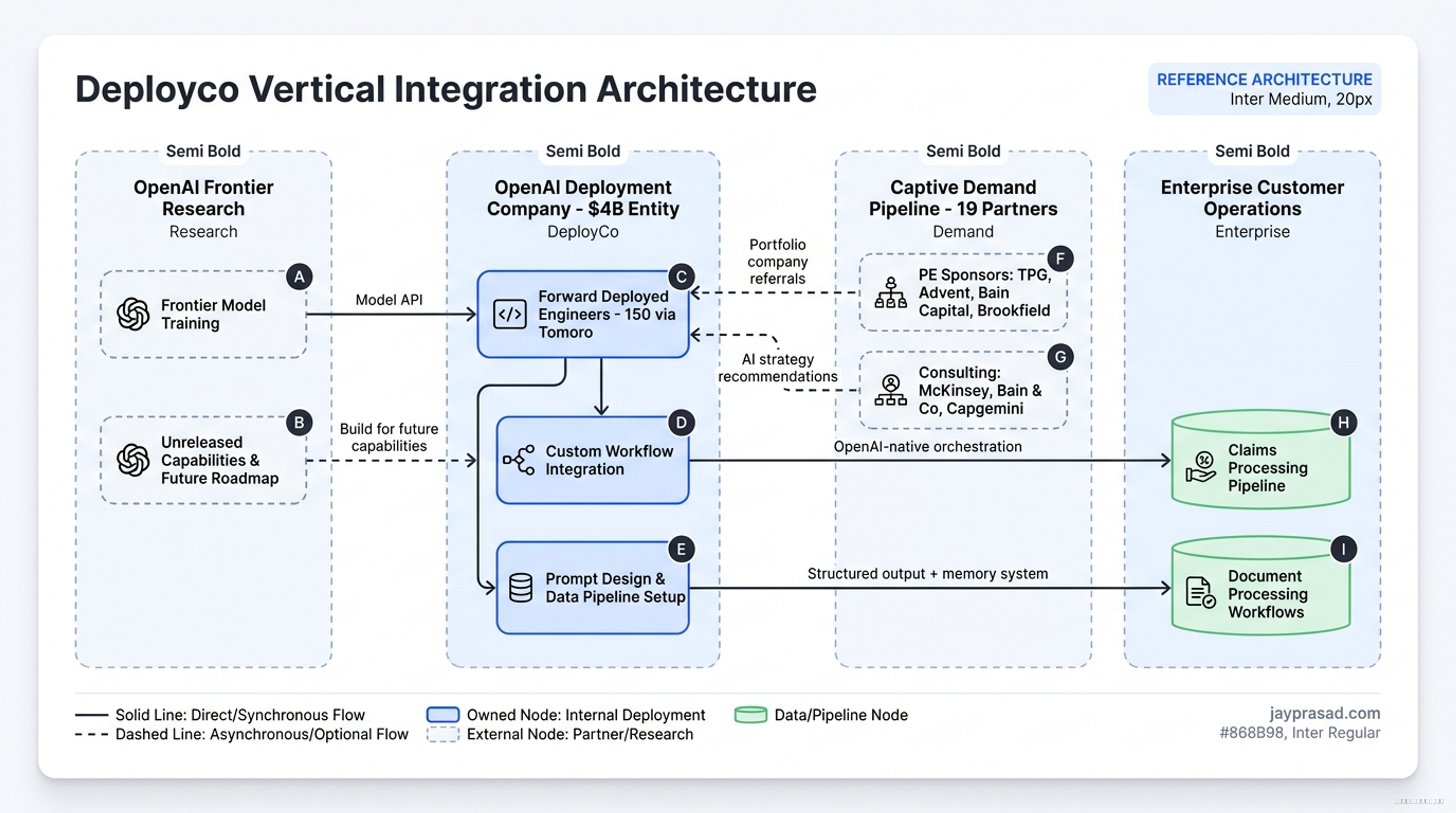

The launch of the OpenAI Deployment Company is being covered as "OpenAI gets into consulting." That framing is wrong. What actually happened: OpenAI built a $4 billion, separately funded entity designed to control everything from frontier model research all the way down to the custom workflow running inside your claims processing pipeline. They recruited 19 investment and consulting partners, including the private equity firms that control thousands of companies, to create a captive demand pipeline no competitor can copy.

This isn't a services arm. It's a platform play disguised as consulting. And if you're an enterprise architect (or aspire to be one), it's the biggest structural shift in enterprise AI since the cloud giants started bundling machine learning services.

---

The Real Problem OpenAI Is Solving (Hint: It's Their Own)

Let's start with the uncomfortable truth. API access is becoming a commodity. Anthropic's Claude, Google's Gemini, Meta's Llama, and a growing ecosystem of open-weight models are all eating away at the pricing power of any single model provider. When your only advantage is "best model," you're one benchmark away from irrelevance.

OpenAI's long-term revenue problem is real. The Deployment Company solves it, not by making better models, but by making it so expensive to leave that it doesn't matter if someone else's model catches up.

The contrarian take: DeployCo isn't about helping enterprises deploy AI faster. It's about solving OpenAI's commoditization problem by burying switching costs so deep into customer operations that model quality becomes irrelevant.

The announcement frames this plainly: "As models become more capable, businesses can apply AI to larger, more important parts of how they operate." Translation: the model is table stakes. The money is in owning the deployment layer.

---

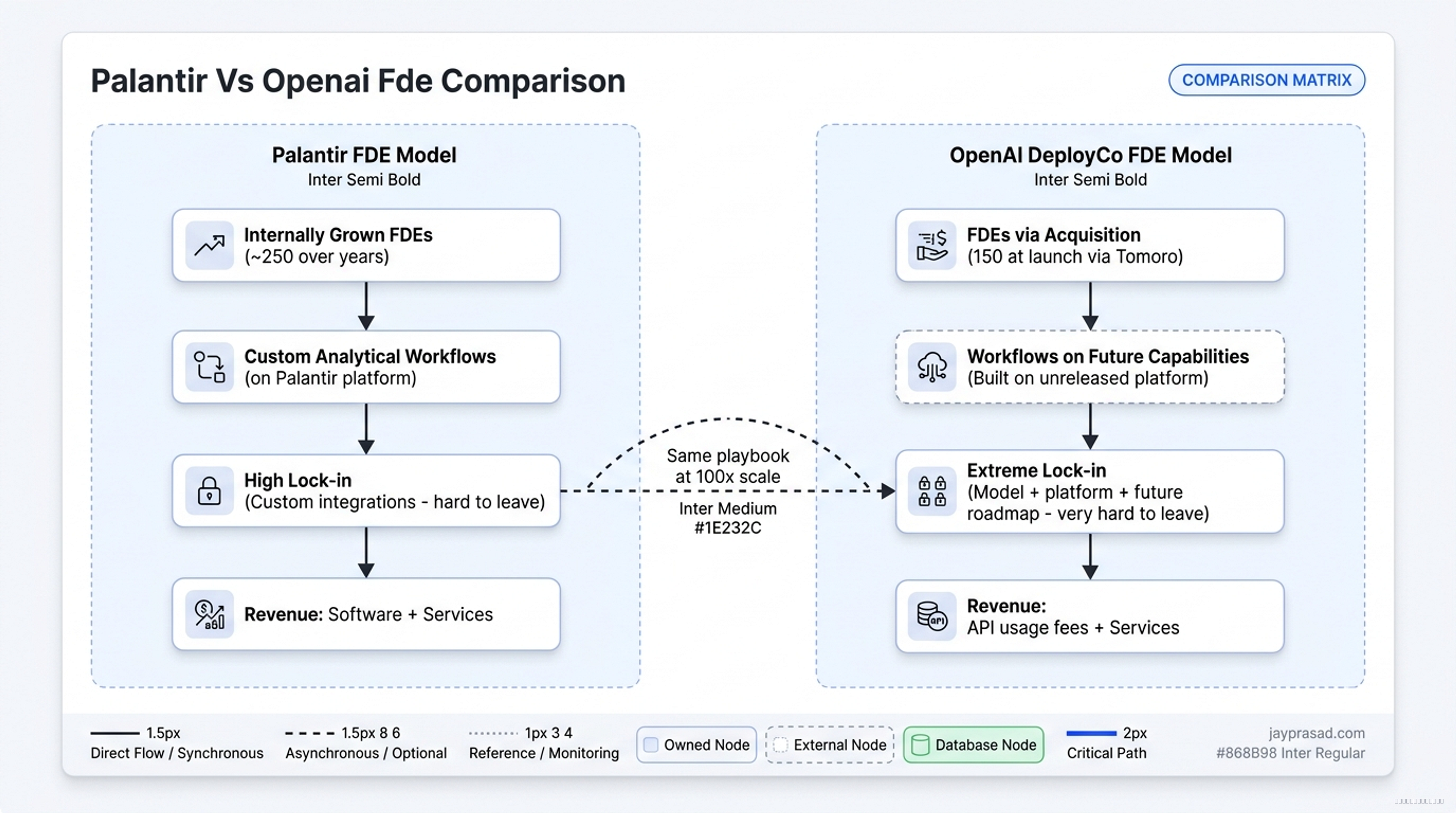

The Forward Deployed Engineer Model: Palantir's Playbook at 100x Scale

The Forward Deployed Engineer (FDE) concept isn't new. OpenAI borrowed it directly from Palantir, which used embedded engineers to build deep operational dependencies inside government and enterprise customers for over a decade.

What Palantir Proved

Palantir's FDE model created enormous value and enormous dependency. Customers got custom-built analytical workflows that no competitor could replicate. But they also got locked into Palantir's platform in ways that made migration practically impossible. Sound familiar?

What OpenAI Is Promising

The announcement contains the most revealing line in the entire press release: FDEs will "build for where OpenAI's frontier capabilities are headed, giving customers systems designed to improve as new models, tools, and deployment patterns come online."

Read that again. Customers are being asked to build critical workflows around capabilities that don't yet exist, from a single vendor.

| Dimension | Palantir FDE Model | OpenAI DeployCo FDE Model |

|---|---|---|

| Scale | ~250 FDEs built over years | 150 at launch (via Tomoro acquisition) |

| How they lock you in | You depend on their platform | You depend on their model + platform + future roadmap |

| Revenue model | Software + services | API usage fees + services |

| Where they find talent | Grown internally | Acquired through buying companies |

| How hard it is to leave | Hard (custom integrations) | Very hard (built on unreleased features) |

The Talent Problem Nobody's Talking About

Vinoo Ganesh, who designed Palantir's Project Frontline program, has been blunt about the scaling challenge: "You can't easily hire your way to a true FDE organization. The skill set is too rare, too specific, too dependent on experiences most engineers never have."

The Tomoro acquisition brings 150 engineers with experience at Tesco, Virgin Atlantic, and Supercell. That's credible. But 150 FDEs against an ambition to transform thousands of enterprises? The math doesn't work without aggressive acquisitions.

Key warning: Every independent applied AI consulting firm with embedded engineering talent is now an acquisition target. If your enterprise AI deployment partner employs fewer than 500 people, you should be actively assessing the risk that they get absorbed into a vendor-aligned entity within 18 months.

---

The PE-Consulting Pipeline: Captive Demand Disguised as an Ecosystem

The partnership structure deserves way more scrutiny than it's getting.

The Money Side

TPG, Advent International, Bain Capital, and Brookfield co-led the $4B+ round. These firms collectively control thousands of companies in their portfolios. When your private equity sponsor is also an investor in the AI deployment firm, the "recommendation" to adopt OpenAI-powered workflows isn't advice. It's a capital allocation decision.

The Advisory Side

McKinsey, Bain & Company, and Capgemini are listed as consulting partners. These are the firms that advise enterprises on AI strategy. They now have a financial relationship with the entity that profits from directing that strategy toward OpenAI.

This has historical precedent. The Accenture-Avanade joint venture with Microsoft created a similar captive demand pipeline in the early 2000s. It persisted for two decades and generated billions in revenue by making Microsoft the default recommendation for every enterprise transformation engagement.

| Partner Type | Firms | What Motivates Them | Risk to You |

|---|---|---|---|

| PE Sponsors | TPG, Advent, Bain Capital, Brookfield | Pipeline of their own portfolio companies | Their "recommendations" carry implicit financial weight |

| Consulting | McKinsey, Bain & Co, Capgemini | Advisory fees + DeployCo economics | Conflict of interest on which model they recommend |

| Model Provider | OpenAI | API revenue + deployment revenue | Controls both the model and the integration layer |

The Independence Question

When a consulting firm advises a client to build AI workflows on OpenAI's stack, and that firm simultaneously profits from that deployment, you have a right to ask: Am I getting objective guidance or a financially motivated referral?

This isn't theoretical. Analysis of enterprise AI failures has found that "failures are almost entirely deployment failures: wrong setup, wrong data pipeline, wrong integration, wrong prompt design. The model isn't the problem." If the model isn't the problem, then the choice of deployment partner matters more than the choice of model. And if your deployment partner has a financial stake in a specific model provider, you've already lost your architectural independence.

---

What This Means for How You Build Your Systems

The architectural implications are where this gets concrete. Let me walk through it.

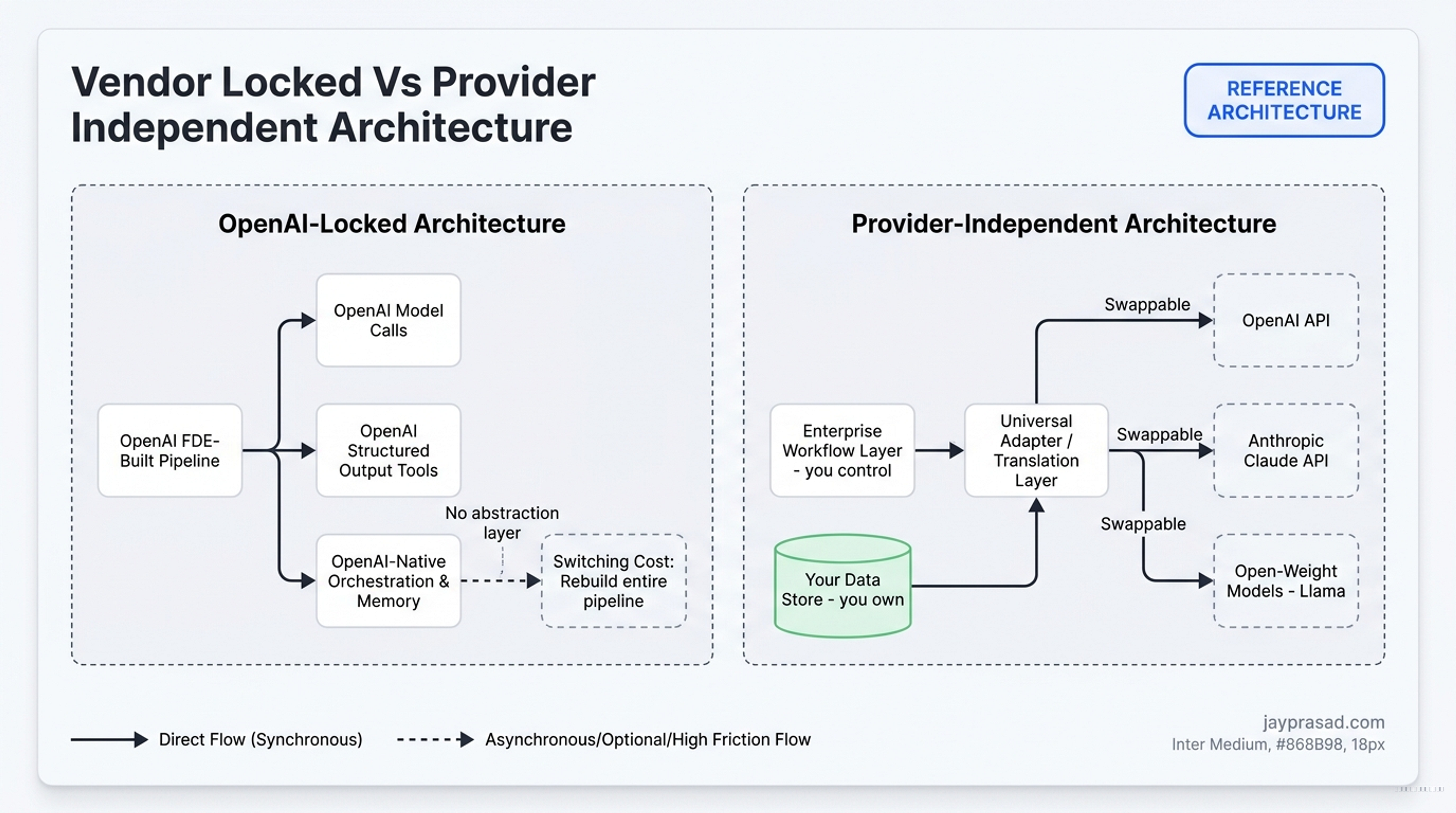

Your Integration Layer Is Now a Strategic Asset

When the same organization that trains the model also controls the prompt design, data pipeline integration, and custom setup inside your production environment, the switching costs become structural rather than contractual. You can't just swap out a vendor. You'd have to rebuild.

Think about what happens when an OpenAI FDE builds your document processing pipeline. Every component in that stack, the model calls, the structured output tools, the orchestration framework, the memory system, is OpenAI-native. There's no middle layer that lets you swap providers. Moving to Anthropic or an open-weight model means rebuilding the entire pipeline, not just changing an API key.

The Provider-Independent Alternative

Now compare that to an architecture that keeps your options open. You put a translation layer (think of it as a universal adapter) between your workflows and whatever model you're using. You use open-source orchestration tools. You store your data in systems you control.

Does this cost more upfront? Yes. Your team has to maintain that adapter layer. But it preserves the ability to swap providers without rebuilding production workflows. That's the tradeoff.

---

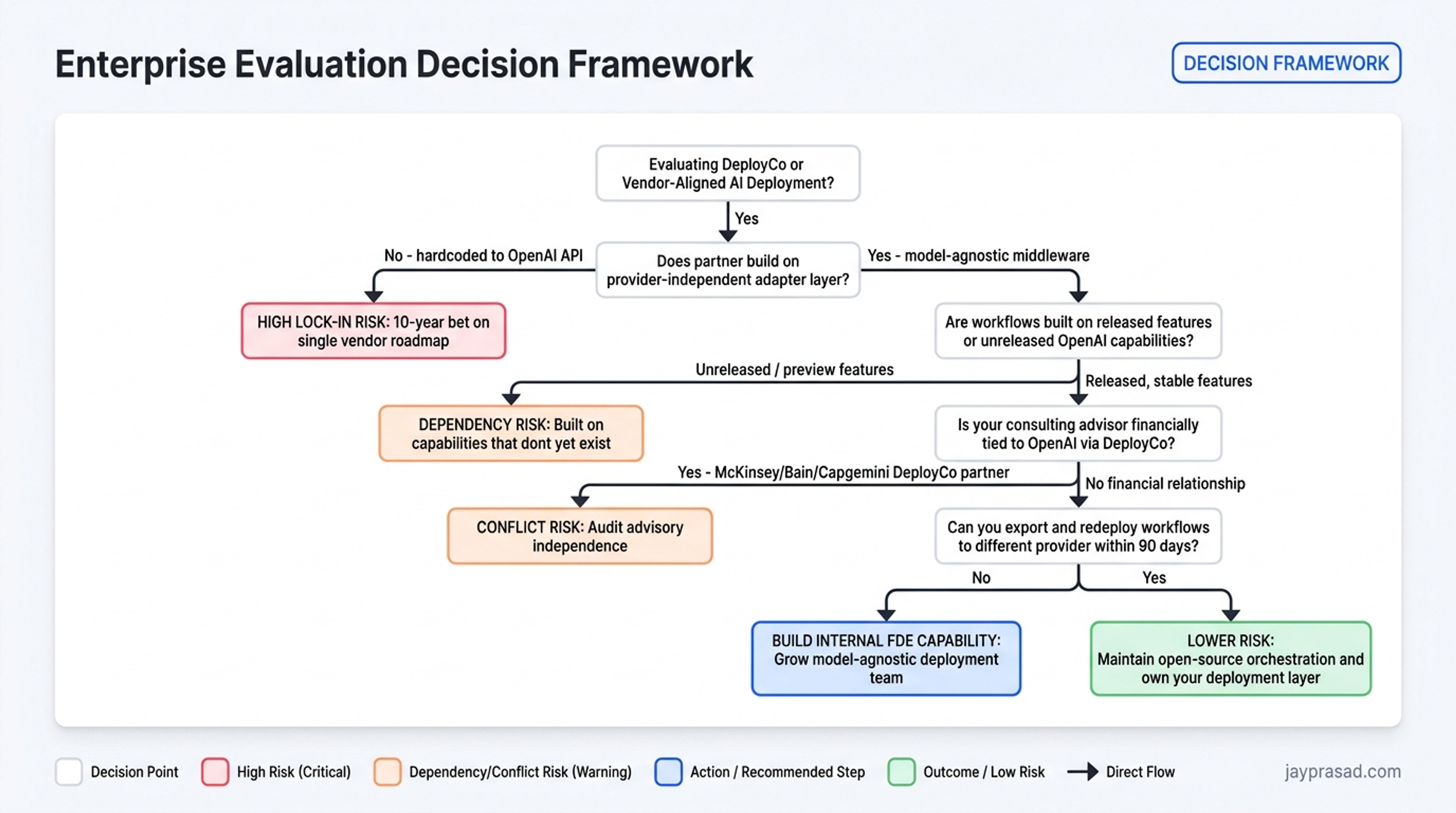

Questions to Ask Before You Sign Anything

If your organization is evaluating DeployCo, or any vendor-aligned AI deployment service, here's what to assess:

- Does the deployment partner build against a provider-independent adapter layer, or does it hardcode to a single provider's API?

- Are custom workflows built on features that are available today, or on unreleased/preview features tied to a specific vendor's future plans?

- Does the consulting advisor recommending this deployment have a financial relationship with the model provider?

- Can you export and redeploy the workflows built by FDEs to a different model provider within 90 days?

- Is your PE sponsor also an investor in the deployment entity? If so, is the "recommendation" truly independent?

- Do you have internal engineering capacity to maintain and evolve the workflows after the FDE engagement ends?

- Are data access patterns and governance controls defined by your architecture team, or by the vendor's FDEs?

---

Anthropic's Counter-Move and What It Tells Us

Anthropic launched a parallel $1.5 billion FDE venture backed by Blackstone and Hellman & Friedman, with zero investor overlap to OpenAI's round. The financial establishment has literally split into two rival camps funding the identical thesis.

This confirms something important: the industry consensus is that the bottleneck for enterprise AI is no longer model quality but deployment execution. Both frontier model providers have independently concluded that owning the deployment layer is existential to their business.

What this means for you: If both OpenAI and Anthropic are racing to own your deployment layer, the smart response isn't to pick a side. It's to make sure neither side owns it. The deployment layer is your competitive advantage, not theirs.

---

The 10-Year Bet You Might Not Realize You're Making

Let me be direct about the decision in front of you.

Letting a single vendor own your deployment layer, from model to orchestration to workflow integration, is a 10-year bet on that company's research trajectory, funding stability, and leadership continuity. OpenAI has had three CEO transitions in two years. Its corporate structure is still evolving. Its competitive position depends on maintaining frontier model leadership against Google, Anthropic, Meta, and a fast-moving open-source ecosystem.

That's a lot of assumptions baked into your production architecture.

The practical path forward:

- Keep a provider-independent orchestration layer. Whether through open-source tools, custom middleware, or competitive FDE relationships, preserve your options.

- Separate deployment from model selection. Your workflow architecture should be a strategic asset you control, not a dependency you inherit.

- Audit advisory independence. If your consulting partner has a financial stake in a specific model provider, factor that into how you weight their recommendations.

- Build internal FDE capability. The skill set is rare, but growing it internally is the only way to ensure your deployment layer serves your interests, not a vendor's.

The era of "just pick the best model" is over. The real battleground in enterprise AI is the orchestration and workflow layer. The organizations that recognize this, and architect accordingly, will be the ones that keep genuine strategic autonomy.

The rest will wake up in three years wondering how they ended up locked into a stack they didn't consciously choose.